Key Highlights

Understanding Interest Rate Cycles and Economic Regimes

Interest rates influence nearly every major financial decision in the U.S. They shape borrowing costs, investment returns, housing affordability, and overall economic growth. Interest rate cycles are not random. They follow repeatable economic patterns. Understanding these cycles helps interpret market behavior, especially in housing, which has historically been one of the most interest rate sensitive asset classes.

What Is an Interest Rate Cycle?

An interest rate cycle refers to the repeated pattern of the Federal Reserve raising or lowering borrowing costs in response to changing economic conditions.

The Federal Reserve operates under what is known as a dual mandate. Its responsibility is to promote maximum employment while maintaining stable prices (Federal Reserve Board).

In practical terms, the Fed attempts to support economic growth while keeping inflation under control.

When inflation rises too quickly or economic activity overheats, the Fed raises interest rates to slow spending and borrowing. When the economy weakens or unemployment rises, the Fed lowers rates to stimulate growth by making credit more affordable.

Because the federal funds rate influences mortgage rates, business lending, and consumer borrowing, these policy changes move through the entire financial system.

Economic Regimes and Rate Cycles

Interest rate movements typically align with broader economic regimes. Each regime creates different investment conditions and housing demand patterns.

Expansion and Stimulus

During economic slowdowns or recessions, the Fed generally lowers interest rates to support recovery. Lower borrowing costs encourage home purchases, business expansion, and consumer spending (Federal Reserve Board).

Following the 2008 financial crisis, the Fed reduced interest rates to near zero and introduced large-scale asset purchase programs known as quantitative easing to stabilize financial markets and improve liquidity (Federal Reserve Bank of St. Louis).

A similar response occurred during the early stages of the COVID-19 pandemic when the Fed again reduced rates to near zero and implemented emergency liquidity measures to support economic stability (Federal Reserve Board).

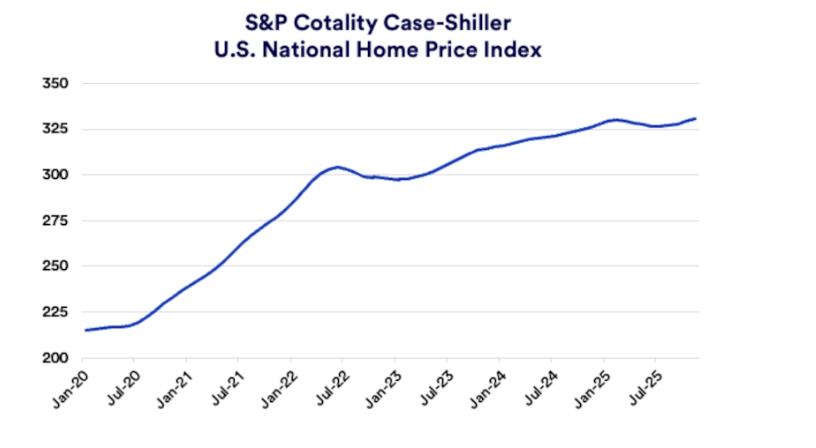

Mortgage rates fell to historic lows, fueling strong housing demand. Between 2020 and 2022, U.S. home prices increased significantly as buyers responded to improved affordability and limited housing supply (S&P CoreLogic Case-Shiller Index).

Stable Growth and Policy Normalization

As economic conditions improve, the Fed typically begins to gradually raise interest rates to prevent inflation from accelerating.

During the mid-2010s, following years of economic recovery after the financial crisis, the Fed slowly increased borrowing costs in an effort to return policy rates to historically normal levels (Federal Reserve Bank of St. Louis).

Housing markets during these periods often transition from rapid price growth toward more sustainable appreciation that is increasingly influenced by local income growth and supply dynamics (National Association of Realtors).

Inflation and Policy Tightening

When inflation becomes elevated, the Fed may increase rates more aggressively. The early 1980s provide one of the most well-known examples. Under Federal Reserve Chair Paul Volcker, the Fed raised interest rates to historically high levels in order to control persistent inflation and restore long-term price stability.

More recently, following pandemic-related stimulus and supply disruptions, inflation reached levels not seen in decades. Beginning in 2022, the Fed raised interest rates at one of the fastest paces in modern history in response to elevated inflationary pressures.

Mortgage rates increased sharply during this period, reducing affordability and slowing housing transaction activity across multiple U.S. markets.

How Housing Markets Typically React

Housing is uniquely sensitive to interest rate changes because most home purchases depend on financing.

Lower interest rates reduce monthly mortgage payments and expand the pool of qualified buyers. This often increases housing demand, accelerates home price growth, and encourages new construction activity (National Association of Home Builders).

Higher interest rates increase borrowing costs and typically slow housing activity. Buyers may delay purchases, transaction volumes decline, and price growth moderates. However, higher rate environments do not always lead to price declines. Supply shortages, population growth, and regional economic strength can still support housing values.

The recent cycle offers a clear example. Record low mortgage rates during the pandemic helped drive rapid home price appreciation. As rates rose between 2022 and 2023, housing affordability tightened and transaction activity slowed, while overall housing inventory remained historically constrained (S&P CoreLogic Case-Shiller Index).

Federal Reserve Chair Jerome Powell has also acknowledged the structural supply challenges affecting U.S. housing. Speaking before Congress in early 2024, Powell noted that elevated mortgage rates combined with historically low existing mortgage rates have created significant market friction.

“The housing market is in a very challenging situation right now. Problems associated with low-rate mortgage lock-in and high mortgage rates, those will abate as the economy normalizes and as rates normalize. But we’ll still be left with a housing market nationally where there is a housing shortage.”

(Jerome Powell, Federal Reserve remarks, as reported by Yahoo Finance)

Powell highlighted that nearly 90 percent of homeowners currently hold mortgage rates below 6 percent, while prevailing mortgage rates remain above 7 percent. This mismatch has reduced resale inventory and contributed to ongoing supply constraints (Yahoo Finance).

Where We May Be in the Cycle Today

While economic cycles never repeat exactly, many economists believe the U.S. economy is transitioning from an aggressive tightening phase toward a more balanced policy environment. Inflation has declined meaningfully from its recent peak but remains modestly above the Federal Reserve’s long-term 2 percent target.

Data suggests inflation has stabilized near the 3 percent range, reflecting easing price pressures across several sectors while housing and energy costs continue to influence overall inflation trends.

Historically, environments like this often represent late-stage tightening or early normalization phases. Housing markets during these transitions typically experience periods of recalibration rather than immediate acceleration, as affordability, supply levels, and consumer confidence gradually adjust.

For long-term investors, these transitional periods often highlight how changing borrowing costs reshape opportunity across asset classes rather than simply signaling short-term market direction.

Why Interest Rate Cycles Matter for Investors

Interest rate cycles influence more than borrowing costs. They shape capital flows, asset valuations, and investor behavior across entire market environments.

Periods of declining rates often support increased investment activity and asset appreciation, while rising rate environments tend to reward disciplined underwriting, supply-constrained markets, and durable income fundamentals.

At Strand, understanding these economic regimes is central to how we evaluate opportunities. Our underwriting focuses on how changing interest rate environments influence housing demand, affordability, and long-term market resilience. This approach allows us to assess investments through a full-cycle perspective rather than reacting to short-term market sentiment.

Housing markets have historically moved in response to cost-of-capital conditions. Investors who understand where the economy sits within a rate cycle are often better positioned to interpret both risks and opportunities as markets evolve.

Final Note

Schedule a meeting with us to discuss how you can benefit from this interest cycle: https://strandcapitalholdings.com/contact-us/